{kind=link}

|

Hearken to this text  |

1X’s Eve robotic.

Over the past a number of years, the funding atmosphere has been robust for robotics startups. Capital deployment has fallen and firms have closed as the overall downturn in tech funding that began in 2022 hit the resource-intensive robotics notably arduous. Now we have tracked that decline — and recognized inexperienced shoots of restoration — in our annual State of Robotics studies.

This yr, nonetheless, the image has modified drastically. Betsy Mule and I had been requested to discuss this altering atmosphere on the RoboBusiness convention earlier this month, and as we close to the yr’s finish we thought it might be value sharing our findings with the broader group.

One of many key drivers of development within the robotics sector has been the falling prices and better efficiency of the know-how’s constructing blocks — issues like computing energy, sensors, motors, and batteries. On the identical time, accelerating advances in AI have been a tailwind for the business.

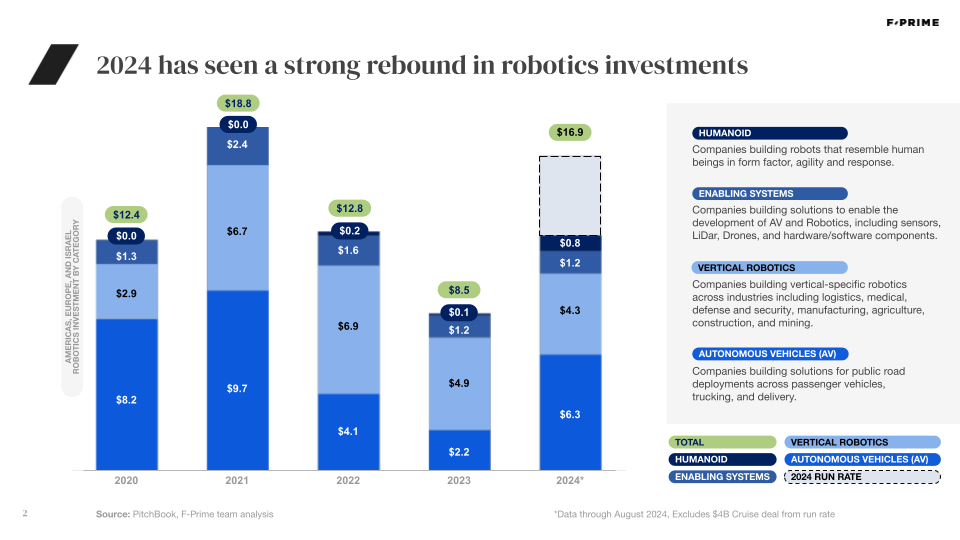

These developments are displaying within the funding information. After a pointy pullback in 2022 and 2023, the primary eight months alone of 2024 have seen a rise in funding over all of final yr, and we count on the complete yr funding exercise to method the all-time highs seen in 2021. On the identical time, firms at totally different levels and throughout totally different industries are seeing sharply totally different funding dynamics play out.

The place is the cash going?

We sometimes break robotics into three core segments; this yr, nonetheless, given the elevated business curiosity and funding in humanoids, we now have damaged them out right into a fourth class of their very own. There was already near $1B of funding in that class by means of August 2024, with firms like 1X, Apptronik, and Determine commanding large funding rounds for general-purpose humanoid kind elements. Buyers embody conventional VCs, company gamers, and AI darlings. In the meantime, some massive companies (like Tesla and Boston Dynamics) are opting to construct their very own humanoids in-house, investing large sums which will even dwarf the enterprise rounds that sometimes make headlines.

In the meantime, after falling off significantly in 2022, autonomous automobile funding as soon as once more accounts for almost all of robotics funding, pushed by company mega rounds and coinciding with a lot of legislative and enterprise milestones. For instance, Waymo reached 100,000 rides per week whereas firms like Aurora have been in a position to develop their operations to new states this yr.

We’ve additionally seen lots of curiosity within the software program layer this yr — notably foundational fashions. Corporations have tried to construct software program for robotics for a while now, however typically run into interoperability, scalability, and reliability challenges. Advances in AI are serving to firms get nearer than ever to overcoming these obstacles, however there are nonetheless challenges. Such fashions must be inherently multimodal, perceive relationships between bodily objects and cause/react when the actual world presents sudden challenges. With enhancements in multimodal giant language fashions, everybody — startups, corporates, teachers — is chasing the one foundational mannequin to rule all of them, although information shortage and different constraints imply we’re removed from a “ChatGPT second” for robotics.

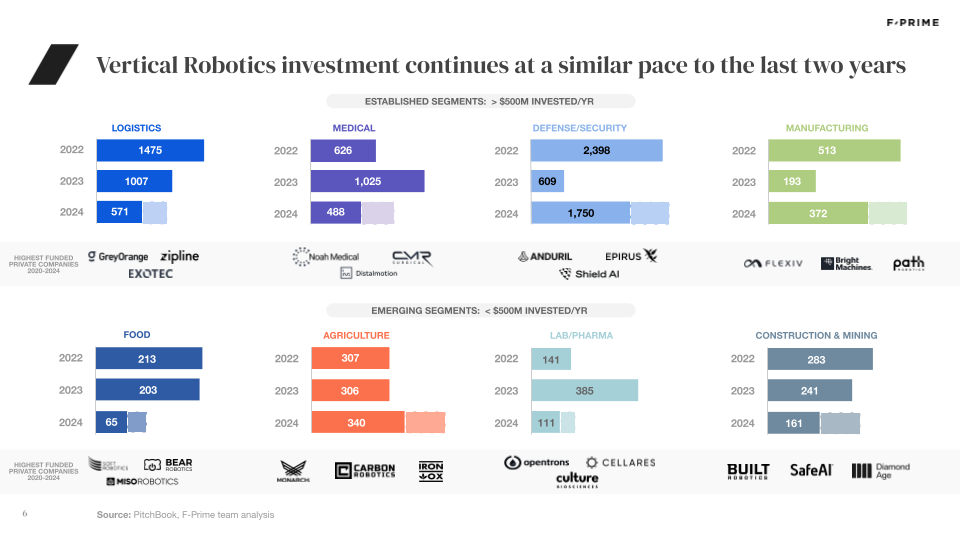

After briefly taking up from AVs as the primary vacation spot for robotics funding in 2022 and 2023, Vertical Robotics continues to develop steadily. Over the past yr, specifically, we’ve seen massive curiosity in purposes for the protection and agriculture industries — see Anduril ($1.5B) and Saronic ($175M) for the previous, and Monarch ($133M) and Carbon ($56M) for the latter.

By stage

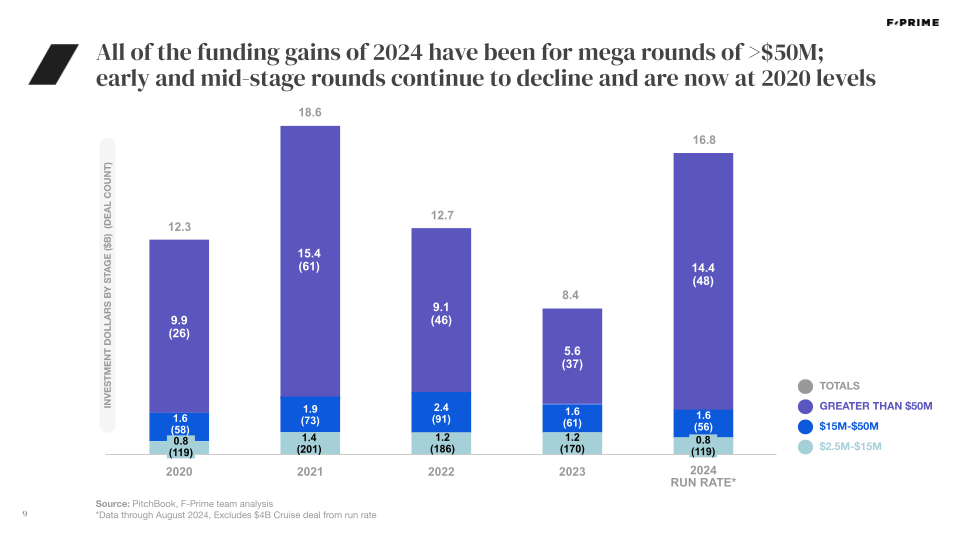

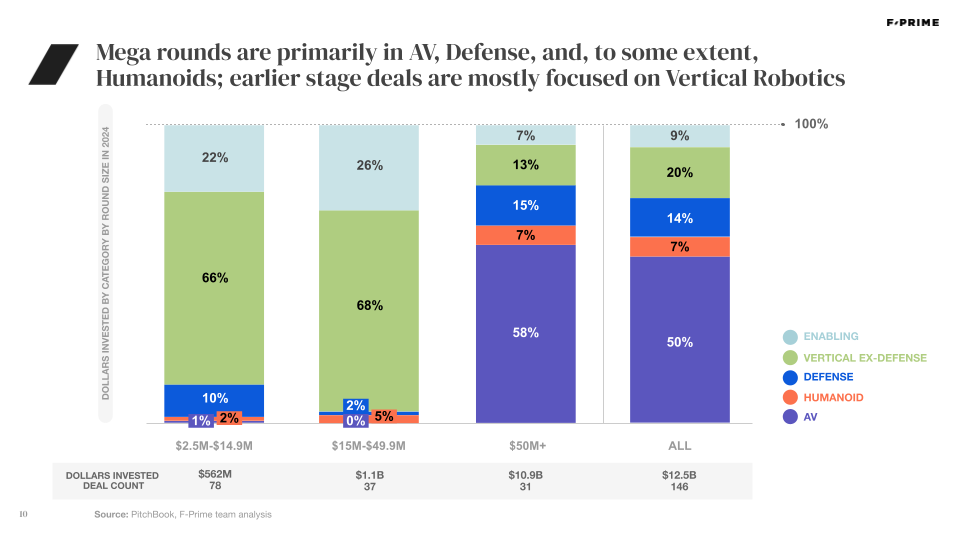

Although funding within the robotics sector has surged, the overwhelming majority of capital has gone to giant, largely late-stage funding rounds. Earlier rounds are literally down year-on-year and again to 2020 ranges. These rounds are additionally a really small portion of the broader enterprise ecosystem. In robotics, earlier rounds account for 15 to twenty % of complete capital, whereas that determine is 20 to 30 % for the broader enterprise ecosystem. The vast majority of the late-stage mega-round funding sometimes flows to AVs, protection and (this yr no less than) humanoids, the vast majority of early stage offers are centered on vertical robotics.

Exit outlook

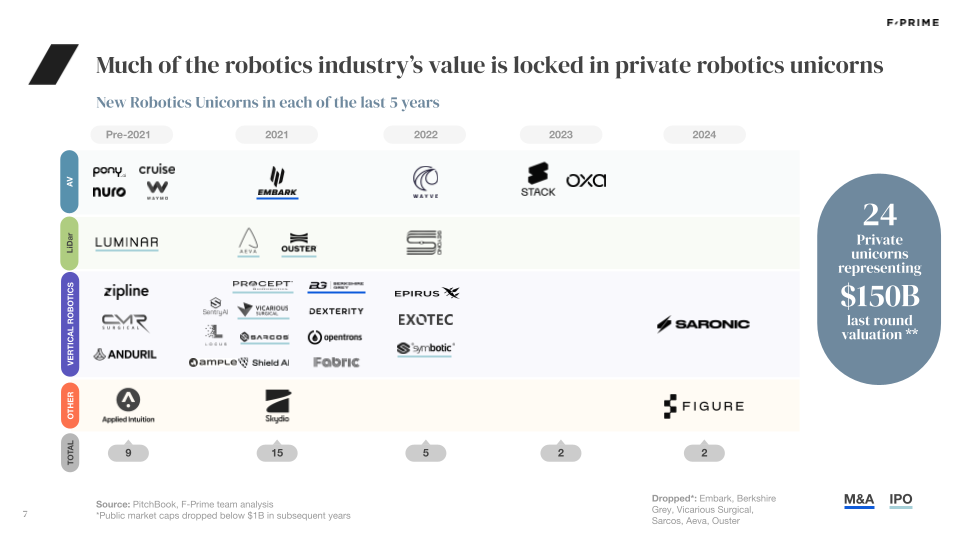

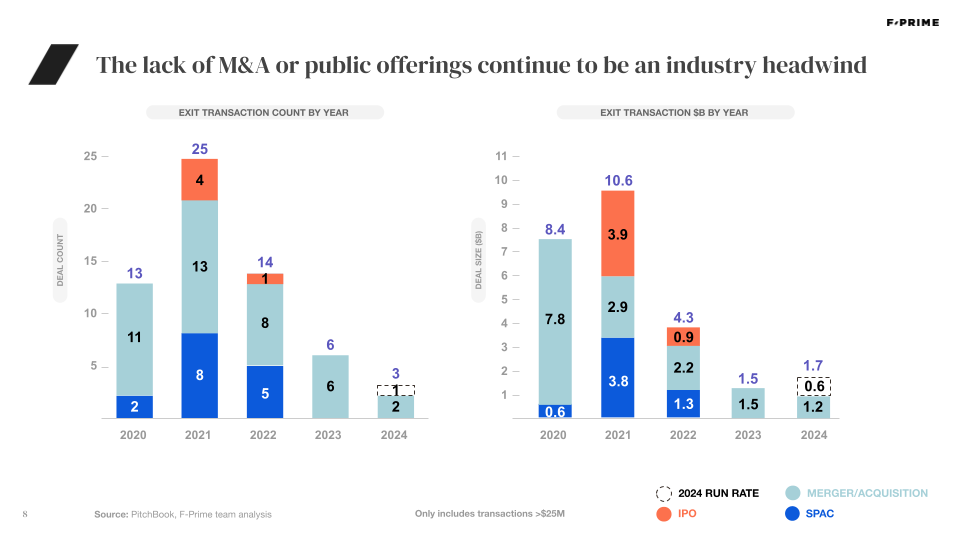

A dearth of profitable robotics exits has created lots of uncertainty round potential returns within the class, and people firms that exited through SPAC or IPO previous to the hunch have carried out poorly within the public markets. A lot of the robotics business’s worth stays locked up in non-public unicorns, and an absence of M&A or public choices proceed to be an business headwind. And amid all of the mega-rounds, we now have additionally seen many well-funded robotics firms shut down or endure restructuring during the last 18 months. Excessive profile shutdowns embody Zume ($446M raised), PrecisionHawk ($139M), Phantom Auto ($95M), and Prepared Robotics ($44M).

Recommendation to founders

The long run tailwinds behind robotics are unmistakable. On the identical time, attracting early-stage investor {dollars} to construct a robotics enterprise is getting more and more difficult. Crossing the gauntlet of delivering excessive ROI, buyer traction, and technical defensibility may be difficult within the early days of any venture-backed enterprise, although it’s notably difficult in robotics the place capital wants are larger and product iteration cycles are longer. Founders have to be laser centered on hitting industrial and technical milestones at each step of the journey, whereas being sensible in regards to the funding atmosphere. Thankfully, for many who handle to cross the gauntlet, there are vital investor {dollars} in search of alternatives to assist construct generational companies in robotics.